The SEC’s Division of Economic and Risk Analysis (DERA) recently released its analysis of custom tag usage in financial filings submitted to the SEC. The analysis covered XBRL financial data submitted with Forms 20-F, 20-F/A, 40-F and 40-F/A from January 2017 to December 2019 by filers preparing their reports using International Financial Reporting Standards (IFRS), which is issued by the International Accounting Standards Board. The analysis focused on trends in filers’ use of custom tags in their XBRL financial data for these forms during the last three years in two categories: 1) Financial statements (F/S) only and 2) F/S and notes.

Thursday, July 30. 2020

IFRS Trend Analysis 2019

When the standard taxonomy does not provide a tag for a necessary financial element, SEC rules permit filers to create custom tags. This customization accommodates unique circumstances in a filer’s particular disclosure. However, the SEC acknowledges that the use of unnecessary customized tags could potentially reduce the comparability of intercompany data. Therefore, the SEC’s rules specify the circumstances under which a filer may create custom tags.

|

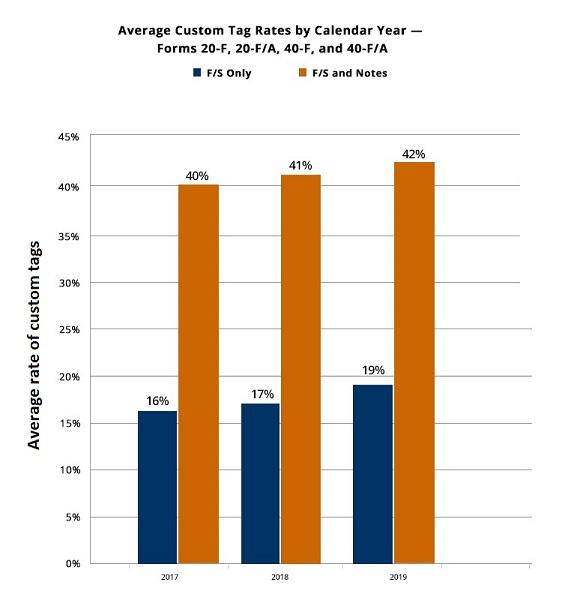

Custom tag usage in Forms 20-F, 20-F/A, 40-F, and 40-F/A from 2017 to 2019 separated by Financial Statements only or Financial Statements and Notes. Source: sec.gov.

The analysis indicates an increase in average custom tag usage from 2017 to 2019, both in F/S and in F/S and Notes. There is an overall larger rate of custom tag usage in F/S and Notes, suggesting usage rates in note information is higher in general.

DERA staff will continue reviewing filers’ use of XBRL custom tags in their submissions to the SEC. The division may share additional trends, issue guidance, or pursue other actions depending on the results of their analyses. For the staff’s previous trend analyses on custom tags, see the Trends section on this page. DERA welcomes questions and comments. Interested parties can contact the Division at (202) 551-5494 or through email at StructuredData@sec.gov.

Sources:

Quicksearch

Categories

Calendar

|

September '25 |

|

||||

|---|---|---|---|---|---|---|

| Mo | Tu | We | Th | Fr | Sa | Su |

| Friday, September 12. 2025 | ||||||

| 1 | 2 | 3 | 4 | 5 | 6 | 7 |

| 8 | 9 | 10 | 11 | 12 | 13 | 14 |

| 15 | 16 | 17 | 18 | 19 | 20 | 21 |

| 22 | 23 | 24 | 25 | 26 | 27 | 28 |

| 29 | 30 | |||||